The global macro environment has entered a delicate and highly sensitive phase, defined by the intersection of three structural forces: exuberance around artificial intelligence-driven corporate activity, pronounced ambiguity in monetary policy direction, and growing fragility within the digital asset ecosystem. Recent AI-related strategic partnerships and investments have temporarily buoyed risk appetite, particularly in select segments of the equity market. This rally rests on thin foundations.

Beneath the surface, investor confidence remains fragile, undermined by inconsistent messaging from Federal Reserve officials regarding the future path of interest rates. This uncertainty is further exacerbated by an ongoing US government shutdown, which has suspended the publication of key economic indicators, from inflation prints to labour market reports, that are essential for informed policy decisions and market pricing. In the absence of reliable data, market participants are forced to navigate by sentiment alone, heightening the risk of dislocations, exaggerated volatility, and asset mispricing across both traditional and digital financial markets.

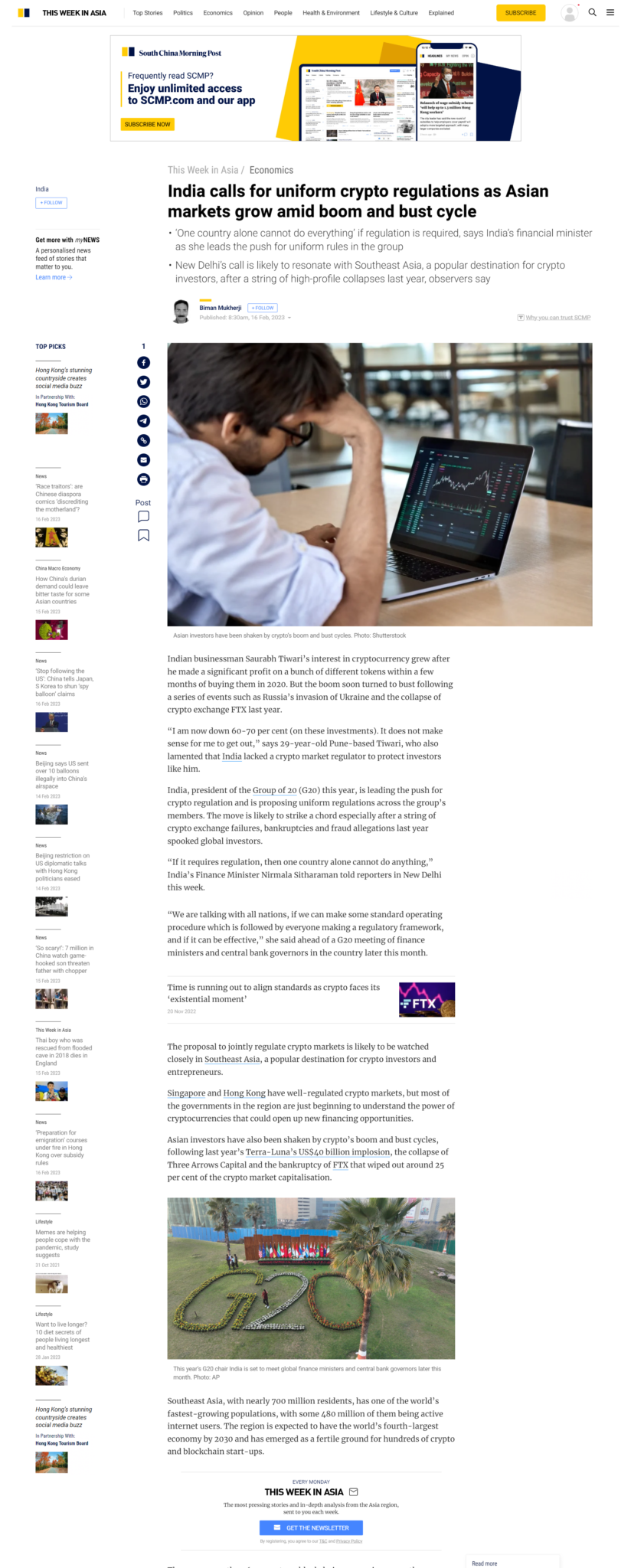

The Reserve Bank of Australia’s decision to hold its cash rate target steady at 3.6 per cent on November 4 aligns with broad market expectations and reflects a global central banking posture of cautious inertia. Without fresh data from the United States, the world’s largest economy, other central banks are reluctant to make bold moves.

Meanwhile, US Treasury yields edged higher, with the two-year yield closing at 3.602 per cent and the 10-year at 4.107 per cent, both rising by 2.9 basis points. This subtle steepening of the yield curve suggests that traders are pricing in a slightly more hawkish near-term stance from the Fed, despite recent rhetoric hinting at potential cuts. The US Dollar Index mirrored this sentiment, climbing modestly to 99.88.

In commodities, gold retreated for a second consecutive day, settling near US$4,000 per ounce. This decline coincided with news that China would end its tax rebate program for certain retailers, a policy shift that could dampen consumer demand and, by extension, reduce safe-haven appetite for the yellow metal. Simultaneously, Brent crude oil held steady at US$64.89 per barrel, as traders digested OPEC+’s decision to pause its planned output increases in the first quarter of 2026. The group’s move reflects growing concern that global demand will soften in the coming months, potentially pushing the market into oversupply territory.

Against this macro backdrop, the cryptocurrency market experienced a sharp contraction, shedding 3.56 per cent in 24 hours to fall from US$3.55 trillion to US$3.42 trillion in total valuation. This decline extends a broader weekly slide of 7.7 per cent, with the Fear & Greed Index plunging to 27, a clear signal of prevailing pessimism. Three interlocking forces drove this selloff: a major DeFi exploit, mounting concerns about Bitcoin’s market cycle, and a renewed correlation with weakening tech equities.

The most immediate catalyst was the US$128 million exploit targeting Balancer V2 pools on November 3. The attack leveraged a flaw in vault access controls, draining assets across multiple chains including Ethereum and Arbitrum. Despite prior audits by reputable firms like OpenZeppelin and Trail of Bits, the protocol’s architecture proved vulnerable to a sophisticated cross-chain manipulation.

In response, Venus Protocol froze BAL collateral, underscoring the systemic risk that one protocol’s failure can pose to the broader DeFi ecosystem. This event shattered the illusion of self-regulation within DeFi, a narrative that had gained traction as the sector matured. With DeFi’s total value locked already down from US$157.5 billion to US$149.6 billion in the week leading up to the hack, institutional investors are likely to adopt a more cautious stance, delaying capital allocation until clearer security standards and regulatory guardrails emerge.

Compounding this technical vulnerability is a growing fear that Bitcoin’s current bull cycle may have already peaked. The asset briefly dipped to US$105,000 on November 4, a level that represents a 16 per cent drawdown from its all-time high. More critically, Bitcoin now trades below its 200-day simple moving average of US$109,882, a key technical threshold that often signals a shift in long-term momentum.

Analysts point to cyclical timing as further evidence of exhaustion: it has been 1,078 days since the November 2022 low, which corresponds to 101 per cent of the typical historical cycle length. With only 45 days remaining in the historical 518 to 580 day window for cycle peaks, the absence of a decisive breakout above US$113,000 suggests that buying pressure is waning. This view is reinforced by outflows from US spot Bitcoin ETFs, which saw assets under management drop by US$13.4 billion month-over-month to US$147.55 billion, indicating that even institutional demand is cooling.

Perhaps most concerning for crypto bulls is the reassertion of a strong correlation with the Nasdaq-100. Over the past 24 hours, the correlation coefficient between Bitcoin and the QQQ ETF reached 0.73, as the tech-heavy index fell 0.8 per cent. This linkage demonstrates that, despite narratives about crypto’s independence, it remains tethered to the fortunes of growth-oriented equities.

While AI-driven deals lifted select stocks, such as Amazon, the broader market remains red, with over 300 S&P 500 constituents in negative territory. This narrow leadership is unsustainable and increases the risk of a broader tech selloff, which would inevitably drag crypto lower. Further eroding Bitcoin’s unique value proposition is its declining correlation with gold, which turned negative at -0.47 over the past 30 days, undermining its status as an inflation hedge.

In summary, the current market environment reflects a perfect storm of technical, cyclical, and systemic pressures. The Balancer exploit exposed foundational weaknesses in DeFi’s infrastructure, shaking investor confidence at a time when Bitcoin’s price action suggests the bull cycle may be running on fumes.

Meanwhile, the rekindled correlation with tech equities ties crypto’s fate to a sector that is itself vulnerable to shifting monetary policy and earnings disappointments. While the Bitcoin RSI has dipped to an oversold 22.63, suggesting a potential short-term bounce, any sustained recovery will require a credible catalyst, most likely a clear dovish pivot from the Federal Reserve.

Until then, traders should closely monitor Bitcoin’s US$105,000 support level and the QQQ’s 630 mark as critical barometers of market direction. In the absence of fresh economic data due to the government shutdown, these technical levels may be the only reliable guides through an increasingly foggy macro landscape.

Anndy Lian is an early blockchain adopter and experienced serial entrepreneur who is known for his work in the government sector. He is a best selling book author- “NFT: From Zero to Hero” and “Blockchain Revolution 2030”.

Currently, he is appointed as the Chief Digital Advisor at Mongolia Productivity Organization, championing national digitization. Prior to his current appointments, he was the Chairman of BigONE Exchange, a global top 30 ranked crypto spot exchange and was also the Advisory Board Member for Hyundai DAC, the blockchain arm of South Korea’s largest car manufacturer Hyundai Motor Group. Lian played a pivotal role as the Blockchain Advisor for Asian Productivity Organisation (APO), an intergovernmental organization committed to improving productivity in the Asia-Pacific region.

An avid supporter of incubating start-ups, Anndy has also been a private investor for the past eight years. With a growth investment mindset, Anndy strategically demonstrates this in the companies he chooses to be involved with. He believes that what he is doing through blockchain technology currently will revolutionise and redefine traditional businesses. He also believes that the blockchain industry has to be “redecentralised”.