The Future of Blockchain

To get a clearer view of the evolution of blockchain in the next decade, as well as the opportunities and threats that the technology will create, we sat down with Anndy Lian, an inter-governmental blockchain expert and book author of Blockchain Revolution 2030.

Regulations and Policy Making

Q: Do you believe in the necessity of unified international laws and regulations regarding blockchain technologies to increase security regarding transactions and data management?

A: That’s a very complex and controversial question. Blockchain technology is a global and decentralized phenomenon that challenges the traditional notions of sovereignty, jurisdiction, and regulation. Different countries have different approaches and attitudes toward blockchain and its applications, especially cryptocurrencies. Some are more supportive and proactive, while others are more restrictive and reactive. There is no global consensus or coordination on how to regulate blockchain technologies, which creates uncertainty and inconsistency for users, developers, and regulators.

“Blockchain technology is a global and decentralized phenomenon that challenges the traditional notions of sovereignty, jurisdiction, and regulation.”

On one hand, some may argue that unified international laws and regulations are necessary to increase security and trust in blockchain transactions and data management. They may claim that harmonized standards and rules would prevent fraud, money laundering, tax evasion, cyberattacks, and other illicit uses of blockchain technologies. They may also suggest that a global regulatory framework would foster innovation, collaboration, and interoperability among blockchain stakeholders and create a level playing field for fair competition.

On the other hand, some may argue that unified international laws and regulations are not feasible or desirable for blockchain technologies. They may contend that blockchain is inherently resistant to centralized control and intervention and that imposing uniform regulations would stifle its diversity, creativity, and potential. They could also point out that different countries have different legal systems, cultures, and values and that imposing a one-size-fits-all approach would violate their sovereignty and autonomy.

Therefore, I think there is no simple or definitive answer to this question. My preference is no.

Anyway, it depends on one’s perspective, interests, and values. I think there are pros and cons to both sides of the argument and that finding a balance between regulation and innovation is a difficult but important challenge for the future of blockchain technologies.

Q: Will regulatory standards and governance undermine the decentralized nature of blockchain or ensure consumer data protection and fraud prevention?

A: That’s another interesting question. I think it depends on the type and degree of regulation and governance that are applied to blockchain technologies. Some regulation and governance may be necessary and beneficial to ensure consumer data protection and fraud prevention, as well as to promote trust, transparency, and accountability in blockchain transactions and data management.

“There is a trade-off between regulation and decentralization, and finding that optimal balance is not easy.”

However, excessive or inappropriate regulation and governance may undermine the decentralized nature of blockchain and compromise its advantages, such as efficiency, security, and innovation.

Therefore, I think there is a trade-off between regulation and decentralization and that finding the optimal balance is not easy. It may vary depending on the specific use case, context, and stakeholder of blockchain technologies. For example, some blockchain applications may require more regulation and governance than others, depending on the level of risk, complexity, and impact they involve. Similarly, some blockchain users may prefer more or less regulation and governance than others, depending on their preferences, expectations, and values.

I think the challenge is to design and implement regulations and governance that are flexible, adaptable, and responsive to the evolving needs and demands of blockchain technologies and their users. This requires a collaborative and participatory approach that involves all relevant actors, such as governments, regulators, developers, users, researchers, and civil society. This also requires a continuous learning and improvement process that monitors and evaluates the effects and outcomes of regulation and governance on blockchain technologies and their users.

Technological and Business Perspective

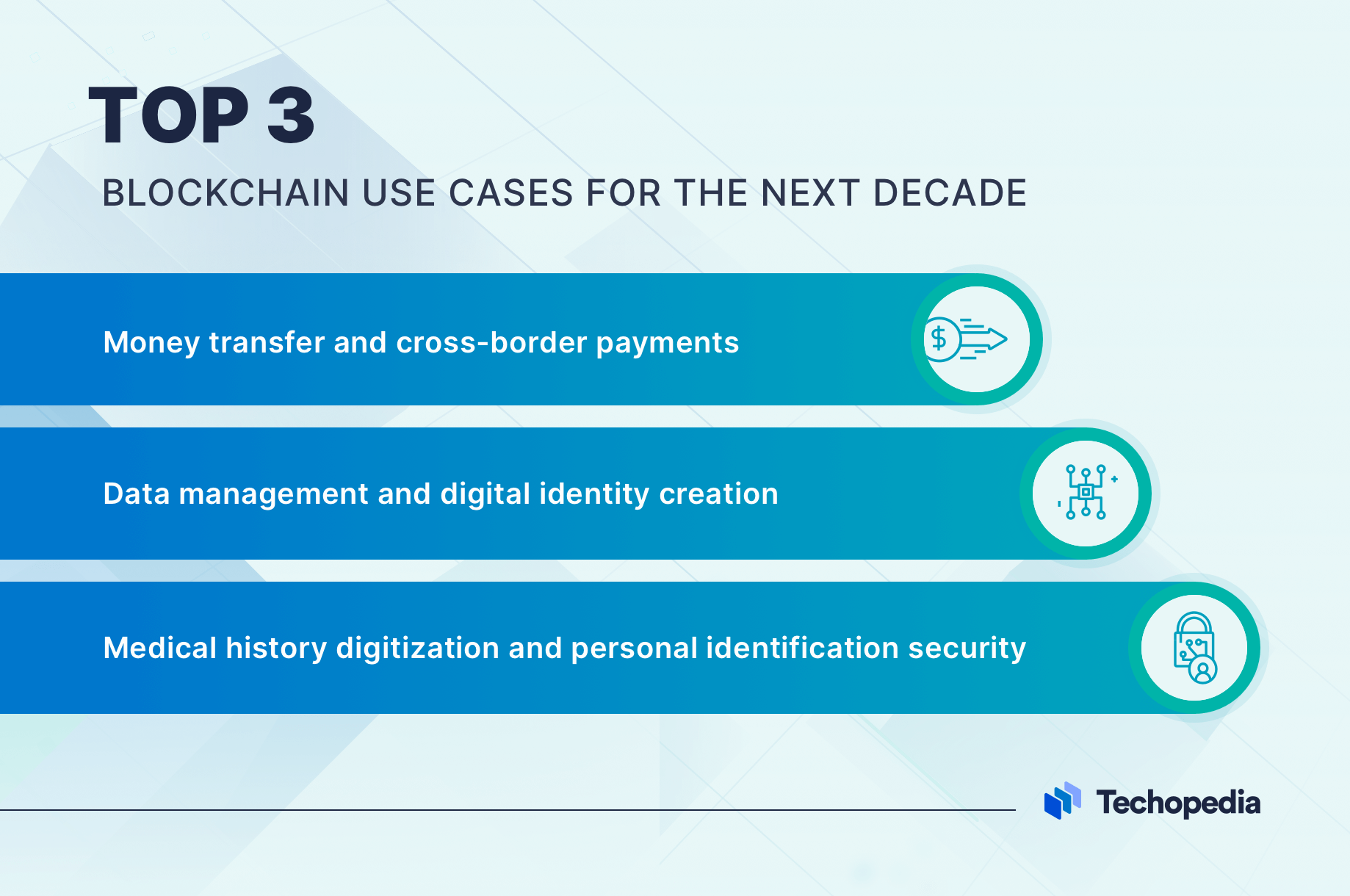

Q: What are the most crucial use cases of blockchain technology for the next decade?

A: Money transfer and cross-border payments. Blockchain technology can enable faster, cheaper, and more secure transactions of money across borders without intermediaries or fees. Blockchain technology can also support the creation and adoption of cryptocurrencies, stablecoins, and CBDCs, which can offer alternative or complementary forms of money to traditional fiat currencies.

Data management and digital identity creation. Blockchain technology can provide a way to store, share, and verify data in a decentralized and immutable manner without relying on centralized authorities or intermediaries. Blockchain technology can also enable the creation and management of digital identities, which can give users more control, privacy, and security over their personal data and online activities.

Medical history digitization and personal identification security. Blockchain technology can help digitize and secure medical records, which can improve the quality and accessibility of healthcare services, as well as protect the privacy and confidentiality of patients. Blockchain technology can also help verify and authenticate personal identification documents, such as passports, driver’s licenses, or birth certificates, which can reduce fraud, identity theft, and human trafficking.

Q: Will smart contracts be highly adopted for trustless financial transactions and extended to stocks, bonds, futures, loans, mortgages, property rights, intellectual property, and other contracts?

A: Yes, smart contracts will be highly adopted for these purposes because they offer more efficiency, security, transparency, and innovation. They may claim that smart contracts can automate and streamline complex and repetitive processes, reduce transaction costs and risks, enhance trust and compliance, and enable new business models and opportunities. They may also suggest that smart contracts can empower users to have more control, choice, and participation in their financial activities.

Q: What opportunities does the convergence of artificial intelligence and blockchain bring?

A: The convergence of artificial intelligence (AI) and blockchain will bring many opportunities for creating new products, services, and solutions that can benefit various domains and industries.

One of the opportunities is to create Web4, which is a term that refers to an intelligent and decentralized web ecosystem that leverages AI and blockchain technologies.

Web4 aims to overcome some of the limitations and challenges of the current web, such as centralization, privacy, security, scalability, and interoperability. It can enable more user-centric, democratic, and collaborative web applications that can empower users to have more control, choice, and participation in their online activities.

Economic Impact

Q: Will blockchain-based financial systems eventually replace traditional financial intermediaries?

A: Blockchain-based financial systems are a relatively new and emerging phenomenon that aims to provide alternative or complementary solutions to traditional financial intermediaries, such as banks, brokers, and exchanges. Blockchain-based financial systems leverage the features of blockchain technology, such as decentralization, transparency, immutability, and programmability, to offer various financial services, such as payments, lending, trading, investing, and insurance.

Some examples of blockchain-based financial systems are cryptocurrencies, decentralized exchanges (DEXs), decentralized finance (DeFi), and central bank digital currencies (CBDCs).

“[There is a view that] blockchain-based financial systems will not replace traditional financial intermediaries but rather coexist or integrate with them.”

Some may argue that blockchain-based financial systems will eventually replace traditional financial intermediaries because they offer more efficiency, security, accessibility, and innovation. They may claim that blockchain-based financial systems can eliminate the need for intermediaries that charge fees, impose restrictions, create bottlenecks and introduce risks. They may also suggest that blockchain-based financial systems can empower users to have more control, choice, and participation in their financial activities.

However, others may argue that blockchain-based financial systems will not replace traditional financial intermediaries but rather coexist or integrate with them. They may contend that blockchain-based financial systems still face many challenges and limitations, such as scalability, usability, regulation, and adoption. In addition, they may point out that traditional financial intermediaries still provide valuable functions and services, such as trust, stability, compliance, and expertise.

Q: Will traditional financial service providers change their business model and embrace blockchain technologies?

A: Yes, traditional financial service providers will change their business model and embrace blockchain technologies because they recognize the value and potential of blockchain technologies for improving their services, processes, and products.

They may claim that traditional financial service providers will adopt blockchain technologies to enhance their customer experience, reduce operational costs, comply with regulatory requirements, and gain a competitive edge. They could also suggest that traditional financial service providers will collaborate with blockchain startups, platforms, and networks to leverage their expertise, resources, and networks.

Q: Will companies that will tokenize their assets get a competitive advantage?

A: I think companies that will tokenize their assets will get a competitive advantage because they will be able to offer more attractive and innovative products and services to their customers, partners, and investors.

They may claim that tokenization of assets will enable companies to create new revenue streams, reduce operational costs, enhance customer experience and loyalty, and access new markets and investors. They could also suggest that the tokenization of assets will give companies an edge over their competitors, who are still using traditional methods of asset management and transfer.

Socio Cultural Impact

Q: Will blockchain technology eventually get widespread adoption? Will people start using and exploiting its potential even without fully understanding how the underlying technology works?

A: It seems that blockchain technology is gaining momentum and recognition among business leaders, but it still needs to overcome some obstacles and uncertainties before it can achieve mass adoption.

Such challenges and risks as regulatory uncertainty, lack of standardization, scalability issues, interoperability problems, and cultural resistance may hinder the widespread adoption of blockchain technology in the near future.

According to a survey by Deloitte, almost 80% of global executives view blockchain as “very important,” and more than 60% of executives believe regulatory issues pose a barrier to blockchain adoption. Another survey by SpendMeNot found that 81% of the 100 largest public companies indicate they use blockchain technology, and 30% of executives believe China will become a blockchain leader by 2023.

As for whether people will start using and exploiting its potential without fully understanding how it works, I think that depends on how user-friendly and accessible the blockchain applications are. Some people may not need to know the technical details of how blockchain works as long as they can trust and benefit from its features. Others may want to learn more about the underlying technology and how it can empower them to create value and innovation.

Trust me. All these are in the works right now. You may not see it, but [blockchain] adoption is on the rise.

Q: We all use the Internet and email but never think about how it works. Will it eventually be the case with blockchain, or is a proper education and understanding of the underlying technology required?

A: Blockchain will be used and implemented without informing you. This is already in the works. Some financial institutions and banks are using blockchain technology to clear the back-end functions that their customers initiate. They do not need to tell everyone about their adoption.

I think blockchain education is important for both users and developers of blockchain applications. Users need to be informed and empowered to use blockchain effectively and responsibly, while developers need to be skilled and innovative to create blockchain solutions that meet the needs and expectations of users.

Threats and Obstacles

Q: What are the major headwinds slowing down the development and further adoption of blockchain technologies?

A: Scalability. Blockchain networks can be slow and inefficient due to the high computational requirements needed to validate transactions. As the number of users, transactions, and applications increases, the ability of blockchain networks to process and validate them in a timely way becomes strained. This makes blockchain networks difficult to use in applications that require fast transaction processing speeds.

Regulation. Blockchain technology is subject to legal uncertainty and regulatory complexity, which can create barriers or conflicts for its adoption and enforcement. Different countries have different approaches and attitudes toward blockchain technology and its applications, especially cryptocurrencies. Some are more supportive and proactive, while others are more restrictive and reactive. There is no global consensus or coordination on how to regulate blockchain technology, which creates uncertainty and inconsistency for users, developers, and regulators.

Acceptance. Blockchain technology is still relatively new and unfamiliar to many people, who may not understand its benefits or trust its features. Blockchain technology also challenges the traditional notions of authority, intermediation, and control, which may create resistance or skepticism from some stakeholders. Blockchain technology requires a cultural shift and a mindset change for its adoption and acceptance.

Q: Sustainability is also a growing concern. Is blockchain able to enhance environmental sustainability?

A: Blockchain technology can enable more effective and accountable climate action initiatives, such as carbon markets, climate finance, or climate governance. Blockchain technology can also enable the creation and exchange of digital tokens that represent environmental values or assets, such as carbon credits, green bonds, or natural capital.

“Start With the Basics”

Q: Anndy, what is your personal advice to those who haven’t yet delved into the world of cryptocurrencies and blockchain technologies? What is the starting point?

A: Start with the basics. Before diving into the technical details or the latest trends, it is important to understand the fundamental concepts and principles of cryptocurrencies and blockchain technologies.

You can start by learning about what cryptocurrencies are, how they work, and why they matter. You can also learn about what blockchain technology is, how it works, and why it is revolutionary.

There are many online courses and resources available for learning about blockchain technology, as well as initiatives that support blockchain innovation in education. I think these are valuable opportunities for anyone who wants to learn more about blockchain and its potential impact.

You can follow Anndy for the latest industry updates on LinkedIn and Twitter.

Source: https://www.techopedia.com/the-future-of-blockchain-anndy-lian

Anndy Lian is an early blockchain adopter and experienced serial entrepreneur who is known for his work in the government sector. He is a best selling book author- “NFT: From Zero to Hero” and “Blockchain Revolution 2030”.

Currently, he is appointed as the Chief Digital Advisor at Mongolia Productivity Organization, championing national digitization. Prior to his current appointments, he was the Chairman of BigONE Exchange, a global top 30 ranked crypto spot exchange and was also the Advisory Board Member for Hyundai DAC, the blockchain arm of South Korea’s largest car manufacturer Hyundai Motor Group. Lian played a pivotal role as the Blockchain Advisor for Asian Productivity Organisation (APO), an intergovernmental organization committed to improving productivity in the Asia-Pacific region.

An avid supporter of incubating start-ups, Anndy has also been a private investor for the past eight years. With a growth investment mindset, Anndy strategically demonstrates this in the companies he chooses to be involved with. He believes that what he is doing through blockchain technology currently will revolutionise and redefine traditional businesses. He also believes that the blockchain industry has to be “redecentralised”.