What do you think of when you hear the words “cryptocurrencies” and “artificial intelligence”? Do you think of innovation and opportunity, or risk and uncertainty? Do you think of the future, or the present? These are some of the questions that Indian Prime Minister Narendra Modi has raised in his capacity as the G20 president, as he calls for a global framework to regulate these technologies and ensure their responsible and beneficial use.

Cryptocurrencies and artificial intelligence (AI) are two of the most disruptive and transformative technologies of our time. They have the potential to revolutionize various sectors and industries, create new opportunities and challenges, and impact the lives of billions of people around the world. However, they also pose significant risks and uncertainties, such as volatility, illicit activities, environmental impact, ethical dilemmas, and social implications. Therefore, it is imperative to have a global framework to regulate these technologies and ensure their responsible and beneficial use.

This is exactly what Indian Prime Minister Narendra Modi has advocated for in his capacity as the G20 president. He has called for international cooperation and guidelines to address the challenges posed by cryptocurrencies and the ethical use of AI. Modi’s push for a unified framework aligns with India’s stance on cryptocurrency regulations, which includes a 30% tax on crypto gains in 2022. It also reflects India’s growing prominence in the field of AI, ranking fourth globally in AI talent.

Modi made these remarks at the B20 Summit in 2023, where he emphasized the need for international rules for cryptocurrencies due to their global impact, comparing it to standardized regulations in the aviation industry. He also highlighted the importance of protecting the interests of all stakeholders, especially the developing and emerging economies, while harnessing the potential of these technologies.

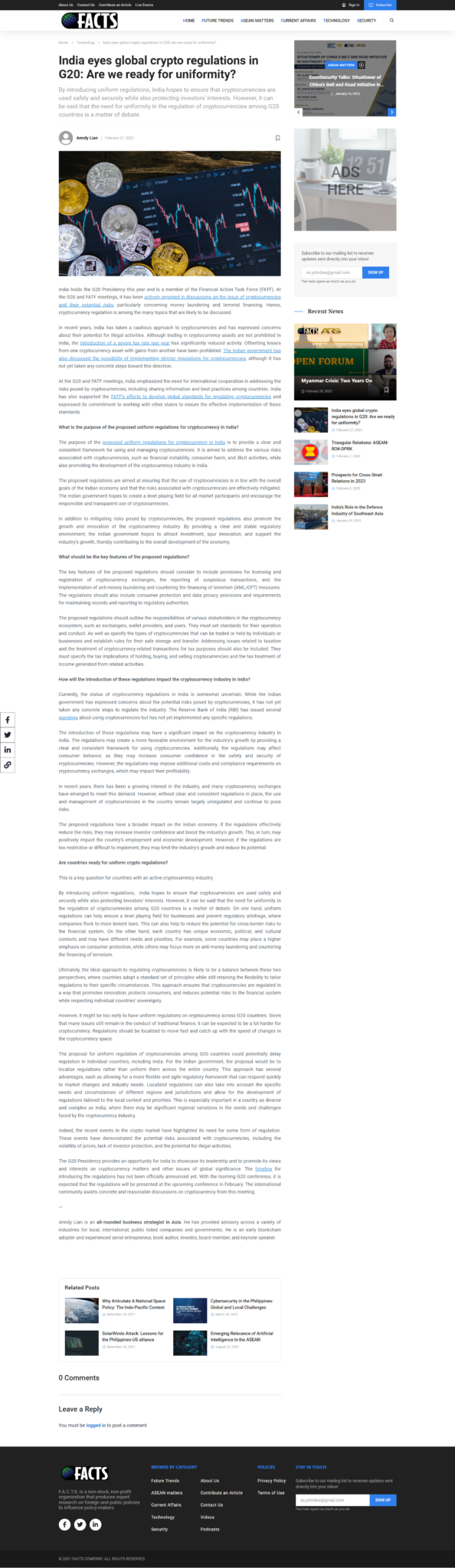

India has been actively participating in the global discussions on crypto regulation, as it holds the G20 presidency in 2023. India has also released a presidency note, which outlines its suggestions for a global framework for crypto assets, based on the guidelines issued by the Financial Stability Board (FSB), the Financial Action Task Force (FATF) and the International Monetary Fund (IMF). The note also emphasizes the need to address the macroeconomic challenges posed by cryptocurrencies, such as volatility, illicit activities and environmental impact.

India’s proactive stance on crypto regulation is commendable, as it shows its awareness of the opportunities and risks associated with these technologies. India has a large and growing crypto market, with over 15 million users and $6.6 billion worth of transactions. India also has a vibrant and innovative crypto ecosystem, with over 300 startups and 10 unicorns. However, India also faces complex legal and regulatory issues regarding cryptocurrencies, such as their status, taxation, KYC norms, consumer protection, and cyber security.

Therefore, India needs to balance its domestic interests with its global obligations. India needs to create a clear and consistent regulatory framework for cryptocurrencies that promotes innovation and growth, while ensuring compliance and accountability. India also needs to collaborate with other countries on creating a common set of standards and rules for cryptocurrencies that foster trust and stability, while respecting diversity and sovereignty.

Furthermore, Modi stressed the importance of integrating rapid technological advancements and protecting stakeholders’ interests. India’s growing prominence in the field of AI, ranking fourth globally in AI talent, makes it a significant player in shaping global discussions on ethical AI and emerging technologies. Modi said that AI has the power to transform various sectors and industries, such as agriculture, health care, education, and manufacturing. He also called for ensuring its ethical use, as it involves human values, rights, and responsibilities.

India has been taking several initiatives to develop responsible AI, such as the National Strategy for Artificial Intelligence and the Responsible AI for Social Empowerment Summit. India has also been collaborating with other countries on advancing AI research and innovation, such as the Global Partnership on Artificial Intelligence (GPAI) and the Indo-French Centre for Applied Mathematics (IFCAM). India has also been supporting various social causes through AI applications, such as disaster management, wildlife conservation, and women empowerment. India’s proactive stance on ethical AI is admirable, as it shows its commitment to contributing to the global dialogue on AI governance and ethics. India has a huge potential to leverage AI for social good, as it has a large population of 1.3 billion people, many of whom face challenges such as poverty, illiteracy, malnutrition, and disease. India also has a rich and diverse culture, which can offer valuable insights and perspectives on AI ethics and values.

Therefore, India needs to balance its technological aspirations with its social obligations. India needs to create a robust and inclusive AI ecosystem that fosters innovation and excellence, while ensuring equity and justice. India also needs to collaborate with other countries on creating a universal framework for ethical AI that respects human dignity and rights, while promoting human development and well-being.

Modi’s push for a global crypto regulation and ethical AI reflects India’s vision of becoming a leader in the digital economy and innovation. It also signals India’s willingness to collaborate with other countries on shaping the future of these emerging technologies. India has a unique opportunity and responsibility to play a pivotal role in the global governance and ethics of cryptocurrencies and AI. India should seize this opportunity and fulfill this responsibility, as it will benefit not only itself, but also the world.

Source: https://wishu.io/modis-push-for-global-crypto-regulation-and-ethical-ai-shows-indias-leadership-in-the-digital-economy/

Anndy Lian is an early blockchain adopter and experienced serial entrepreneur who is known for his work in the government sector. He is a best selling book author- “NFT: From Zero to Hero” and “Blockchain Revolution 2030”.

Currently, he is appointed as the Chief Digital Advisor at Mongolia Productivity Organization, championing national digitization. Prior to his current appointments, he was the Chairman of BigONE Exchange, a global top 30 ranked crypto spot exchange and was also the Advisory Board Member for Hyundai DAC, the blockchain arm of South Korea’s largest car manufacturer Hyundai Motor Group. Lian played a pivotal role as the Blockchain Advisor for Asian Productivity Organisation (APO), an intergovernmental organization committed to improving productivity in the Asia-Pacific region.

An avid supporter of incubating start-ups, Anndy has also been a private investor for the past eight years. With a growth investment mindset, Anndy strategically demonstrates this in the companies he chooses to be involved with. He believes that what he is doing through blockchain technology currently will revolutionise and redefine traditional businesses. He also believes that the blockchain industry has to be “redecentralised”.